Decision Making Framework [ Part 2]

Decision Making Framework [ Part 2]

The Second Five Elements [Premium Readers Only]

[Premium Readers Only]

If you haven't read part 1 yet, get acquainted with that first as this piece is a continuation. Also do hit me up if you have any frameworks of your own which you think are worth sharing. This journey is all about learning after all!

6 Exit Plan

Deciding when to exit and investment play is arguably the most important part of the whole process. Gains and losses are not realised until the investment is closed. For instance, say I bought an ETF to reflect trends in global population change and had a rocky period where the value of my investment was now worth 20% less than inception. This theoretical loss will only be locked in once the position in the ETF is sold. However, if I rode the storm and later down the line saw the value of my investment become worth 20% more than inception then similarly, this theoretical gain would not be real until the ETF is sold. However, this doesn’t mean that the losses/gains are not real, just that the investment has to be closed in order for the impact to hit the pockets. Something can easily go down and never come back up.

Personally, there are three reasons why I unwind/sell an investment. Let me explain:

Theme - if the underlying reason for making an investment doesn’t exist anymore or my resultant thesis is outright wrong, then I have no credible reason to stay invested. I’d be fooling myself. If I have to sell at a loss then so be it. I can handle being wrong, it happens. Sometimes, there could be a better method of expressing a theme that involves selling one ETF and buying another.

Timing - if my holding period (set out from inception) has expired then it is generally time for me to sell. For instance, my recovery based themes are somewhat time dependent. So naturally, if the timing expires then it is a sign for me to sell. Most of my recovery exposures will be closed when we actually have a sustained post covid recovery (more details shared during the upcoming ETF Deep Dive Series).

Life Emergency - I’ve had one life emergency so far that has meant I needed way more money than was in my ‘rainy day’ pot. I drawed down on my investing pot without hesitation because what’s the point of making money if I can’t use it when it really matters. Family was my primary concern and money was secondary. I had to rebuild my pot but that was fine, there are many more things to be thankful for!

7 Sizing

When I decide which ETF to buy an important question is how much to spend? You will notice that I like simple approaches when it comes to personal investing because it shouldn’t be an activity that gives me too much stress. There are elements of complexity which I will always aim to explain clearly but mostly I will try to keep to straightforward concepts. I only invest amounts that does not impact my ability to cover the costs of my day to day life (plus a bit of playtime). So except in the case of an unpredictable emergency, my ETF pot can exist without me having to drawdown from it.

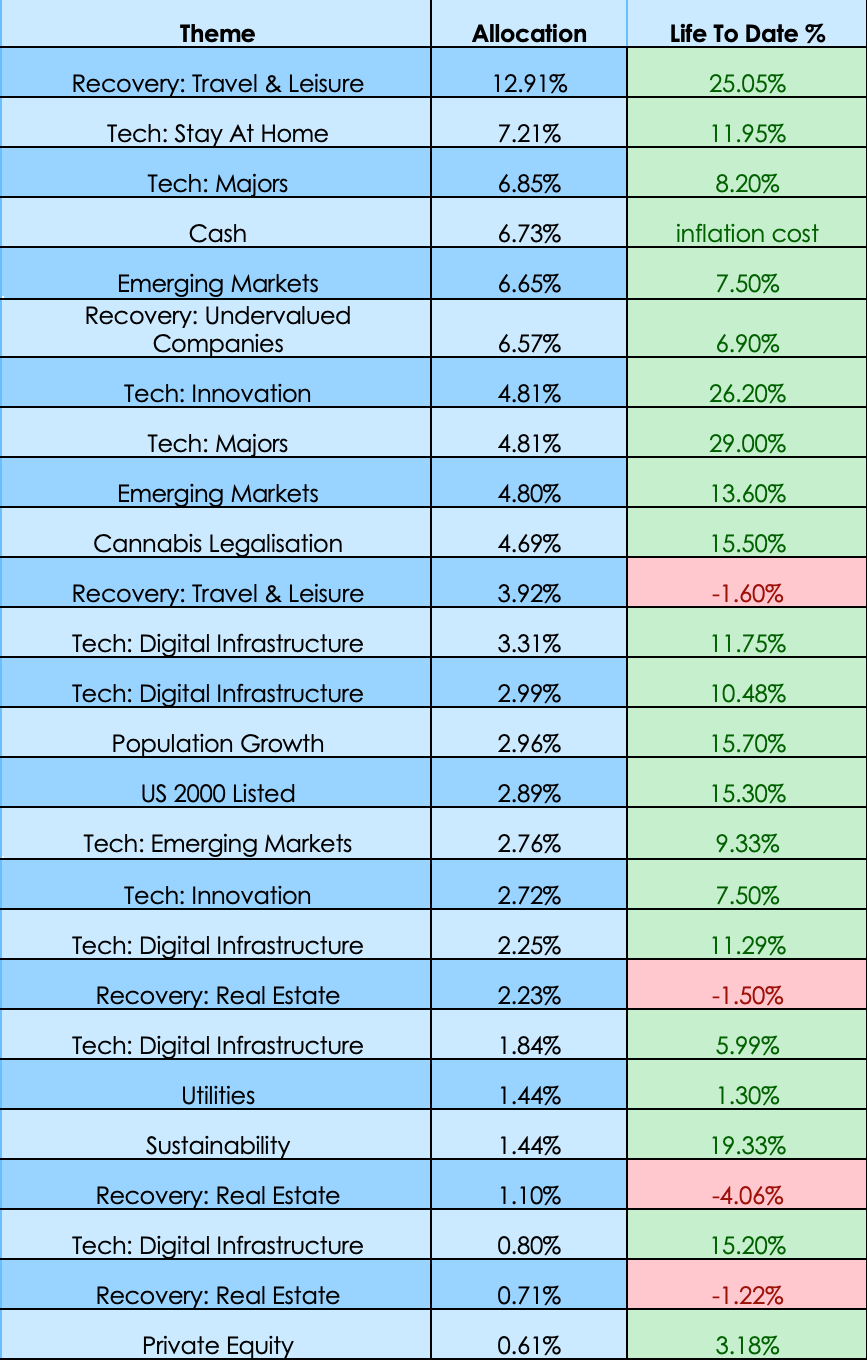

When it comes to sizing individual holdings, I take the perspective of the portfolio overall in percentage terms.

For instance my thematic breakdown as of the end of December ‘20 was as follows (I will update this in detail for you, the premium readers only, later this month):

Rules of Thumb I Use For Discipline:

Maximum Risk Contribution: Worst Case = -10% of total portfolio*

Maximum Theme Weight: 50% of total portfolio value

Maximum SIngle ETF Weight: 25% of total portfolio value

Minimum Theme Weight: 5% of total portfolio value

Minimum SIngle ETF Weight: 2.5% of total portfolio value

Let me explain this further as it is essentially the golden rule for myself, I may compromise on the others at times but never for risk contribution. I posit that, if the worst case scenario (as discussed in part 1) of a single ETF position results in a loss bigger than 10% of the whole portfolio then I must make the position smaller.

Here’s an example:

Total Portfolio Value: £30,000

Example ETF Size: £5,000

Worst Case Scenario: -50%

Risk Contribution: -£2,500 or -8.33% i.e. 2500/30000 = 0.083

This would be within my overall tolerance of -10% but imagine I had a position size of £7,500 instead:

Total Portfolio Value: £30,000

Example ETF Size: £7,500

Worst Case Scenario: -50%

Risk Contribution: -£3,750 or -12.5% i.e. 3750/30000 = 0.125

Now this would be beyond my risk tolerance so clearly I’d have to reduce the size. But what if I was super convicted about an idea and wanted the biggest position possible?

Total Portfolio Value: £30,000

Maximum Risk Contribution: -10% or -£3,000

Maximum Size: £6000 derived from -£3,000 divided by 50% i.e. 3000/0.5

This is a simplistic approach, risk management at an institutional scale is much more complicated but it’s enough for me not to stress about my portfolio. Having an idea of my worst case scenario losses helps to minimise the noise. It’s important to recognise that investing is inherently risky and all my positions can experience their worst case scenarios at the same time, especially if they are related themes!

8 Correlations

Correlation describes the statistical relationship between two or more things. In this context, I care about how similar or dissimilar my ETF positions behave day to day.

For example, two ETFs could share the same driver of returns i.e factors and consequently share similar directional patterns. In simple terms, they go up and down together. Correlations have a scale of 1 to -1 to help describe whether a relationship is +ve or -ve. ETFs with high correlation (closer to 1) will move in the same direction most of the time while ETFs with low correlation will move in opposite direction most of the time (closer to -1).

I don’t compute these every time, again institutions do this in much depth. However, I bear this in mind when thinking about which themes to align with. The more related the themes are, the more likely my portfolio will experience higher volatility (as defined by how widely dispersed returns are i.e. bigger difference between up and down days). Some people like to have highly correlated investments which is fine and some people prefer less volatility (remember this is just one assessment of volatility) which is also fine.

Example Portfolio 1

Portfolio Size:ETF (A) = 50% ETF (B) = 50%

Correlation:+1 or simply ‘two related themes’

Returns Day 1: ETF (A) = +2% ETF (B) = +2%

Returns Day 2:ETF (A) = -2% ETF (B) = -2%

Portfolio Returns Day 1:(50% x 2%) + (50% x 2%) = 2%

Portfolio Returns Day 2: (50% x -2%) + (50% x -2%) = -2%

Example Portfolio 2

Portfolio Size: ETF (A) = 50% ETF (B) = 50%

Correlation: -1 or two unrelated themes

Returns Day 1: ETF (A) = +2% ETF (B) = -2%

Returns Day 2: ETF (A) = +2% ETF (B) = 2%

Portfolio Returns Day 1: (50% x +2%) + (50% x -2%) = 0%

Portfolio Returns Day 2: (50% x -2%) + (50% x +2%) = 0%

Which portfolio is more volatile based on the examples?

Anyway, before we fall down a rabbit hole, the point is that I ask myself how related are the themes I am exposing myself to and whether I am comfortable. More correlation means the likelihood of all my holdings experiencing bad days at the same time will be higher. The more intertwined the themes are, the more volatility I should expect - including bigger down days!

9 Timing

This is a tough part of the process because it depicts the buy low | sell high mantra that is at the core of every good decision but simultaneously the hardest thing to perfectly time.

For instance, the best time to buy and asset is obviously before it rockets higher but there is no 100% perfect way of timing this. People can get lucky (I definitely got lucky last year) but generally there is a bit of pain/losses to experience before things go up. An even harder pill to swallow is that I could have a theme/thesis that plays out correctly and I still don’t make money on my investment because of timing or other things outside of my control. For me, the best way to try and make my own luck is to participate consistently over time and use a framework that I can try to improve on over time. The biggest advantage I have is my age, being in my 20s means I have a LONG time to benefit from the long term investing process. I chose to be more aggressive in the short term so I have to be comfortable with having a rocky road towards my goals. We are investing at all time highs after all.

Nevertheless, when making a new investment, I assess where I am on the trend timeline. The further I am from catalysts, the more likely I am to deploy my whole size then sit back and see how things play out. But if the theme has played out significantly and there are no better alternatives, then I’d probably drip feed into the investment over time. For example, buying an equal amount over some time period.

10 ETF Profile

This will probably require a separate publication but I will try to be succinct. The final piece of my decision making process is to analyse the profile of the ETF in question. The elements I care about are as follows:

Costs: remember ETF stands for exchange traded fund. There are numerous costs associated with running an ETF normally given as an expense ratio charged annually. The more specialised an ETF is the more expenses it is likely to incur i.e. closer to 1% while the tracker style ETFs tend to be cheaper i.e. circa 0.2% and below.

FX Exposure: the first layer is the currency which the ETF is denominated in, many of my ETFs are denominated in USD and it is down to the investor (me in this case) to hedge the fx risk, which I don’t.

The second layer is the currency of the ETFs holdings itself. For instance, it may own foreign companies denominated in say Japanese Yen. Some fund managers will hedge this FX and their ETFs tend to be a bit more expensive, others don’t.

Concentrated Exposures: although most of the ETFs I own usually hold 20+ companies, they could have a high concentration in one or a handful of companies. I need to be aware of this as that company/companies would be a larger driver of overall returns from that ETF. If I am not comfortable I may decide to find an alternative with a more diverse holding.

Rebalancing Frequency: ETFs are essentially massive investment portfolios which have specific goals and risk management protocols. Financial markets are super dynamic if they do not make adjustments, the risk parameters of the fund could change such that it no longer reflects the overall aims.

For example, let’s imagine the following:

An ETF aims to invest in 5 high growth US technology companies as defined by US revenues above 70%

Company A 80%

Company B 90%

Company C 60%

Company E 95%

Company F 100%

As we can see, Company C no longer fits the criteria so the fund manager will have to sell it and find a replacement. They may schedule this change straight away or at specified points during the year instead. If I intend on being strict on my exposures at any given point in time then this is a key consideration because technically an ETF can be slightly out of sync with its aims at times. Generally though, fund managers seek to minimise tracking error and tracker based ETFs are far more strict with rebalancing. Thematic ETFs are a lot more discretionary.

Accumulating vs Distributing: just as some companies pay dividends to their shareholders, ETF managers will usually set up in one of two ways: reinvest income earned or pay it out to fundholders. At the moment my aim is not to generate income but instead to maximise compounding effects and growth so I select accumulating style ETFs only.

Impact on Portfolio: this ties back in with my earlier point about sizing. the most important thing is to make sure each additional ETF does not exceed my risk contribution tolerance nor break my maximum/minimum weighting rules. This helps me stay sensible and not overexpose myself to one investment.

I hope you find this useful for constructing or challenging your own decision making frameworks. In the premium readership pipeline, I will be publishing a blog series exploring specific ETFs as I look for ways to better align with themes so look out for that!

Catch you later,

Peace.